What Is Address Verification? AVS, USPS & Proof Of Address

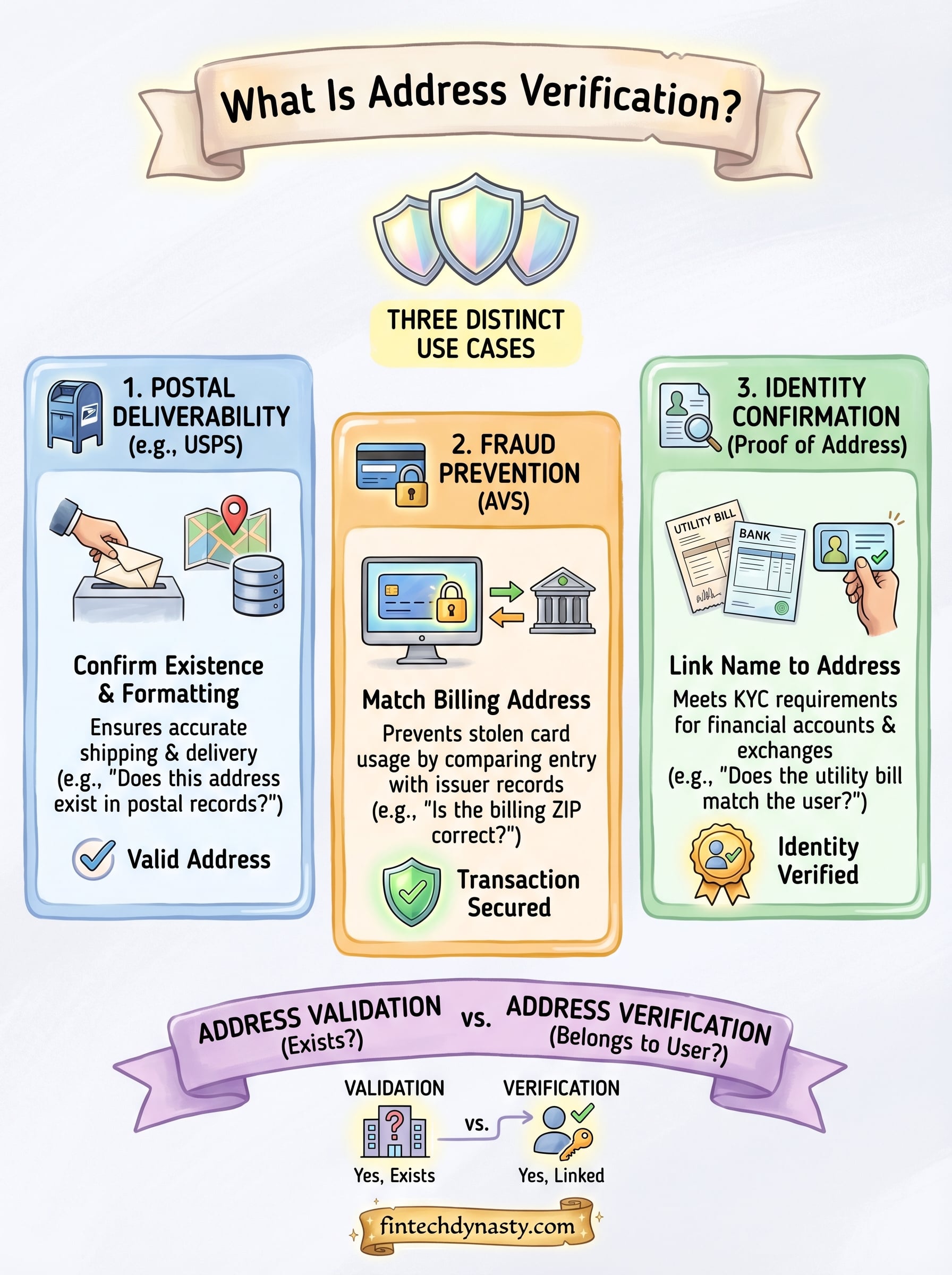

Address verification is a process used to confirm that a physical address is real, accurate, and associated with the person providing it. It sounds simple, but the term actually covers three distinct use cases: postal deliverability through services like USPS, credit card fraud prevention through the Address Verification System (AVS), and identity confirmation through Proof of Address documents.

If you're managing cryptocurrency through self-custody or interacting with exchanges that require KYC, you've likely encountered at least one form of address verification already. Exchanges ask for Proof of Address documents before letting you withdraw funds. Payment processors run AVS checks when you buy a hardware wallet online. These systems exist to prevent fraud and verify identity, two things anyone holding digital assets should care about deeply.

This article breaks down each type of address verification, explains how they work, where they apply, and why they matter, whether you're confirming a shipping address, processing a card transaction, or completing identity verification on a crypto platform. At FinTech Dynasty, security education goes beyond seed phrases and cold storage; understanding the verification systems around you is part of protecting your assets too.

Why address verification matters

Understanding what is address verification helps you recognize why so many systems rely on it. Fraud costs businesses and individuals billions of dollars each year, and unverified addresses are one of the most common entry points. Whether someone submits a false billing address to use a stolen card or provides fabricated documents to open a financial account, address verification acts as a gate that stops bad actors before damage is done. The more accurately a system confirms that an address is real and tied to the right person, the harder it becomes to exploit.

Protecting payments and reducing chargebacks

When you buy something online, the merchant's payment processor runs a quick check to see if the billing address you provided matches what the card issuer has on file. This check is called the Address Verification System (AVS), and it exists specifically to catch stolen card usage. Merchants who skip AVS expose themselves to chargebacks, which happen when a cardholder disputes a transaction they didn't authorize.

A single chargeback costs a merchant far more than the original transaction value once fees and administrative costs are factored in.

For you as a buyer, AVS also protects your card from unauthorized use. It makes it harder for thieves to complete fraudulent purchases using your card details without knowing your billing address, adding a practical layer of protection you benefit from every time you check out online.

Meeting KYC requirements on crypto platforms

If you use a centralized exchange, you've almost certainly been asked to submit Proof of Address documentation as part of the Know Your Customer (KYC) process. Regulators require exchanges to verify that users are who they say they are, and a valid address document such as a utility bill or bank statement is one of the key pieces of that puzzle.

Failing to complete this step blocks your ability to withdraw funds or increase trading limits on most platforms. For anyone serious about self-custody and asset security, understanding why platforms demand address verification helps you move through the process faster and with less friction.

How address verification works in practice

When you ask what is address verification, the mechanics matter as much as the definition. Each system works by comparing the address you provide against a trusted reference source, then returning a result that tells the receiving party whether the data matches, partially matches, or fails.

Matching data against trusted records

In a postal context, services like USPS compare your submitted address against the official Delivery Sequence File, which contains every valid deliverable address in the United States. The system standardizes formatting, fills in missing ZIP+4 codes, and flags addresses that don't exist in the database.

For card payments, the comparison happens between the billing address you enter at checkout and the address your card issuer has stored on your account.

The issuer returns a match code to the merchant's payment processor, which uses that code to decide whether to accept, flag, or decline the transaction. The entire exchange takes a fraction of a second.

What happens when verification fails

A failed verification doesn't always mean fraud. Typos, outdated address records, and formatting differences cause many legitimate checks to return a partial match or no match. The system gives the receiving party a signal, but a human decision or fallback process usually determines what happens next.

For identity verification on a crypto exchange, a failed address check typically triggers a manual review. Your submitted document gets evaluated by a compliance team before your account access is updated.

Address verification vs address validation

These two terms often get used interchangeably, but they describe different processes with different goals. Understanding what is address verification versus validation clarifies the distinction quickly. Address validation checks whether an address is real and correctly formatted. Address verification goes further and confirms that the address belongs to the specific person providing it.

What address validation does

Address validation is a technical formatting check. It confirms that a street, city, and ZIP code combination exists in a postal database and follows the correct structure. If you mistype your street name or enter an invalid ZIP code, validation catches the error before it causes a delivery failure. It works entirely without identity context.

Most e-commerce checkout forms run address validation automatically in the background. The process has nothing to do with who you are.

What address verification adds

Verification requires a human or document in the loop. It links an address to a specific individual by cross-referencing submitted documents or card records against what a bank, issuer, or government database holds.

Validation tells you the address exists; verification tells you the address belongs to the person behind it.

For anyone using a crypto exchange or buying a hardware wallet online, both processes apply. The checkout form validates your shipping address automatically, while the KYC process verifies that your Proof of Address document matches your identity on file.

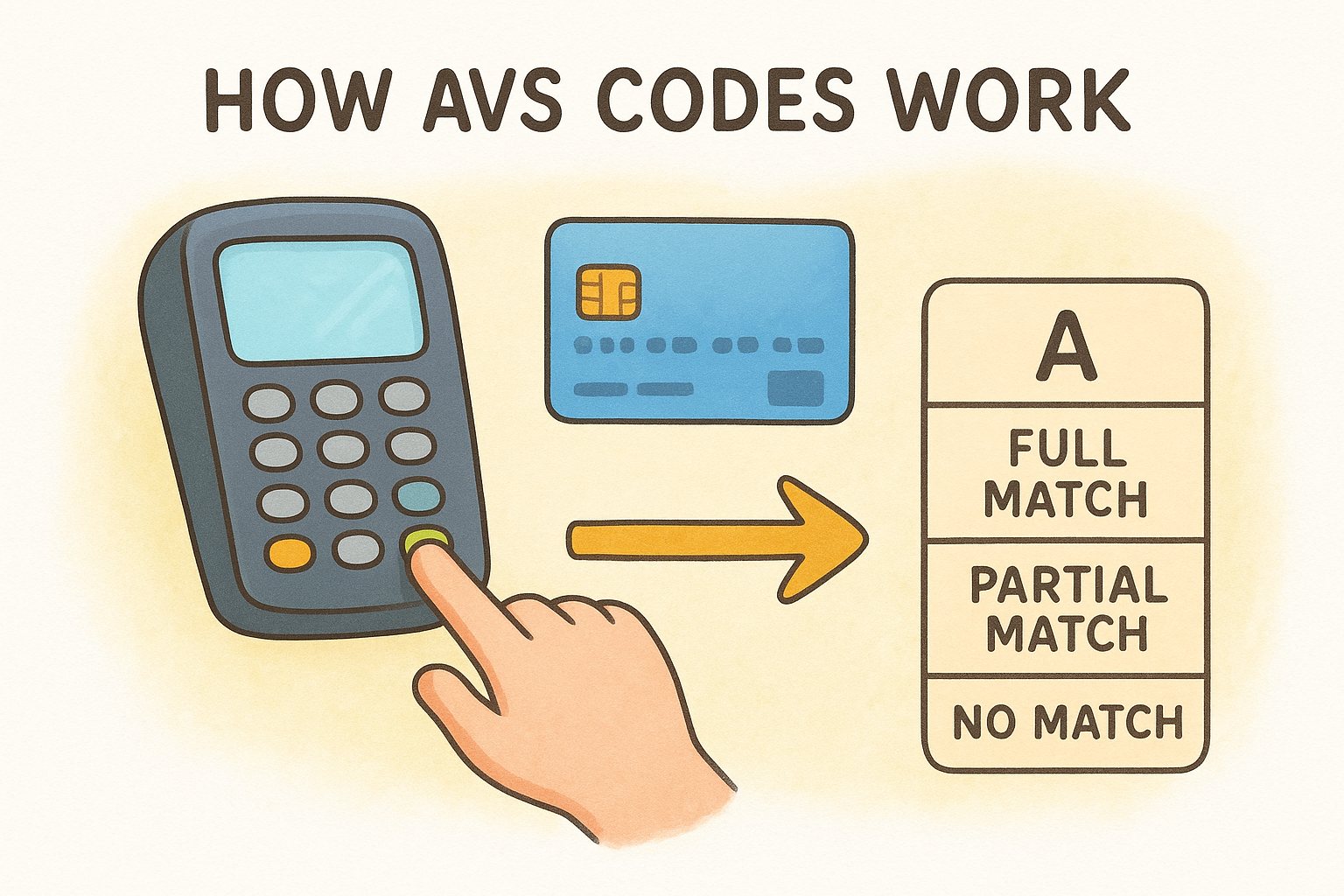

AVS for card payments

The Address Verification System (AVS) is a fraud-detection tool built into credit and debit card processing. When you enter your billing address at checkout, AVS sends that data to your card issuer, which compares it against the address tied to your account. The result comes back as a single letter code that tells the merchant whether the address matched, partially matched, or failed entirely.

Merchants use AVS codes to decide whether to approve a transaction, flag it for review, or decline it outright.

How AVS codes work

AVS returns specific response codes that represent different match outcomes. A full match means your street number and ZIP code both aligned with your card issuer's records. A partial match typically means one element matched and the other didn't. Knowing what is address verification in this context shows you why a correct billing address matters at checkout, not just a valid card number.

Here are the most common AVS result categories:

- Full match: Street number and ZIP code both match

- Partial match: Only ZIP code or only street number matches

- No match: Neither element aligns with issuer records

- Unavailable: The issuer doesn't support AVS for that card

AVS limitations you should know

AVS only checks billing address components, not the full street name or city. That narrow scope means a fraudster who knows your ZIP code and house number could still pass an AVS check. International cards present another gap since many non-US issuers don't support AVS at all.

Merchants who rely solely on AVS take on unnecessary exposure. Combining it with CVV verification and device fingerprinting creates a stronger barrier. Keeping your billing address current with your bank ensures AVS works correctly every time you check out.

Proof of address for identity checks

Proof of Address (POA) is the document-based side of what is address verification. When a crypto exchange or financial institution asks you to verify your identity, they require you to submit a physical document that links your full name to a current address. This step is separate from postal validation or payment fraud prevention; it confirms who you are and where you live as part of a KYC compliance requirement.

Documents that qualify as proof of address

Most platforms accept a narrow list of official documents for this type of verification. The document must typically show your full name, current address, and a recent issue date, usually within the last 90 days.

Common accepted documents include:

- Bank statements

- Utility bills (electricity, gas, or water)

- Government-issued correspondence

- Mortgage or lease agreements

An expired document or one older than 90 days will almost always trigger a rejection, so check the date before you submit anything.

What happens after you submit

Once you upload your document, the platform's compliance system or review team compares it against the personal details already stored in your account. If your name and address match your registered information, your verification tier updates and access restrictions lift. A mismatch sends your submission to manual review, which can delay withdrawals or account upgrades by several business days. Keeping your address current on all financial accounts prevents that kind of friction before it starts.

Key takeaways

Understanding what is address verification means recognizing that the term covers three separate systems with distinct purposes. Postal verification confirms that an address exists and is deliverable. AVS protects your card transactions by comparing your billing address against your card issuer's records. Proof of Address documentation satisfies KYC requirements on exchanges and financial platforms by linking your name to a current, physical address.

Each system adds a direct layer of protection that works in your favor. Keeping your billing address current with your bank, submitting recent documents for identity checks, and understanding why platforms request this information puts you in control of the process rather than caught off guard by it. Security in crypto extends beyond seed phrases and cold storage. If you want a structured path through wallet management, self-custody, and broader crypto security fundamentals, start with the FinTech Dynasty crypto education course and build your knowledge from the ground up.