Acceptable Documents for Proof of Address (Banks & DMV)

Whether you're opening a bank account, updating your driver's license, or completing KYC verification on a crypto exchange, you'll almost certainly be asked to provide acceptable documents for proof of address. It's one of the most common identity requirements across financial institutions, and one that catches people off guard when they don't have a utility bill handy.

At FinTech Dynasty, we help people take control of their digital assets through self-custody and proper security practices. But before you can buy your first hardware wallet or move crypto off an exchange, you often need to verify your identity and address with that very platform. Understanding which documents qualify saves you time and frustration.

This guide breaks down every valid proof-of-address document accepted by banks, the DMV, and government agencies, along with alternatives if you don't have the usual paperwork. We'll also cover how to obtain these documents when you're starting from scratch.

Why proof of address matters in the US

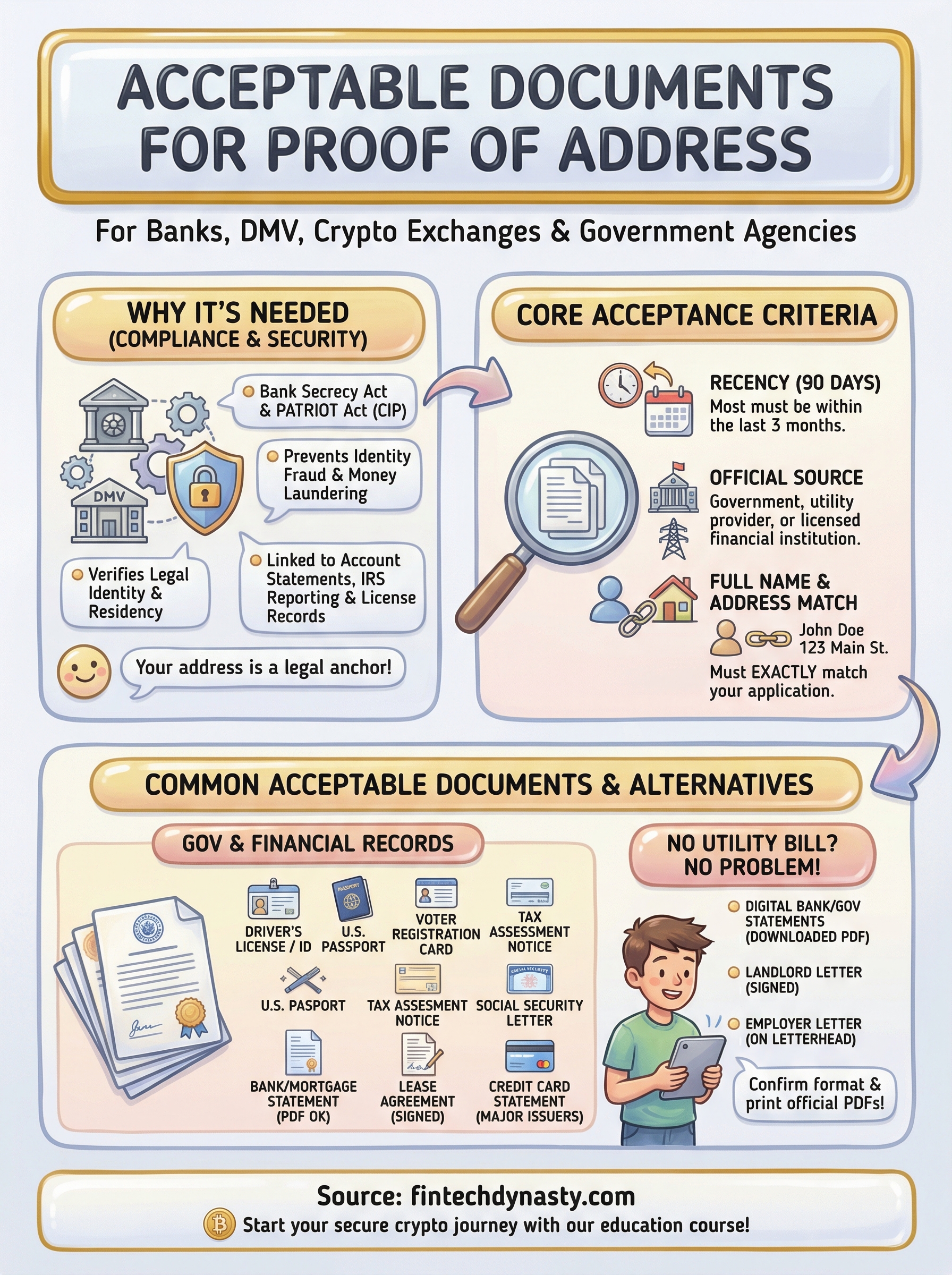

In the United States, address verification is tied directly to federal anti-money laundering regulations and identity fraud prevention. Financial institutions, government agencies, and even crypto exchanges are legally required to confirm that you are who you say you are and that you actually reside where you claim. This is not optional paperwork; it is a compliance requirement built into the financial system, and institutions that skip it face heavy regulatory penalties.

The regulatory requirement behind address verification

The Bank Secrecy Act (BSA) and the USA PATRIOT Act require financial institutions to collect identifying information from every customer, including proof of a current residential address. This falls under what is formally called a Customer Identification Program (CIP). When you open a bank account or complete verification on a crypto exchange, the institution must document that your address was confirmed through a recognized, reliable source before you gain full access.

Failing to provide acceptable documents for proof of address does not just slow down your application; it can result in outright rejection or a frozen account.

What institutions actually do with your address

Your residential address serves several functions beyond a basic identity check. Banks use it to mail statements, report accounts to the IRS, and flag suspicious activity tied to geographic inconsistencies. The DMV links your address to your license record so it can send renewal notices, registration updates, and any legally required correspondence. Crypto exchanges use it to meet international KYC standards, which means an unverifiable or foreign address often triggers additional review steps.

Institutions also use address data to detect fraud and identity theft. If someone attempts to open an account using your address without your knowledge, the verification trail becomes a key point of investigation. Your address, at its core, is the physical anchor that connects your legal identity to a real location in the world.

What makes a document acceptable

Not every piece of mail with your name on it qualifies as acceptable documents for proof of address. Institutions look for documents that meet specific standards around recency, official origin, and reliability before they will process your request. Knowing these criteria upfront prevents you from wasting time submitting paperwork that gets rejected.

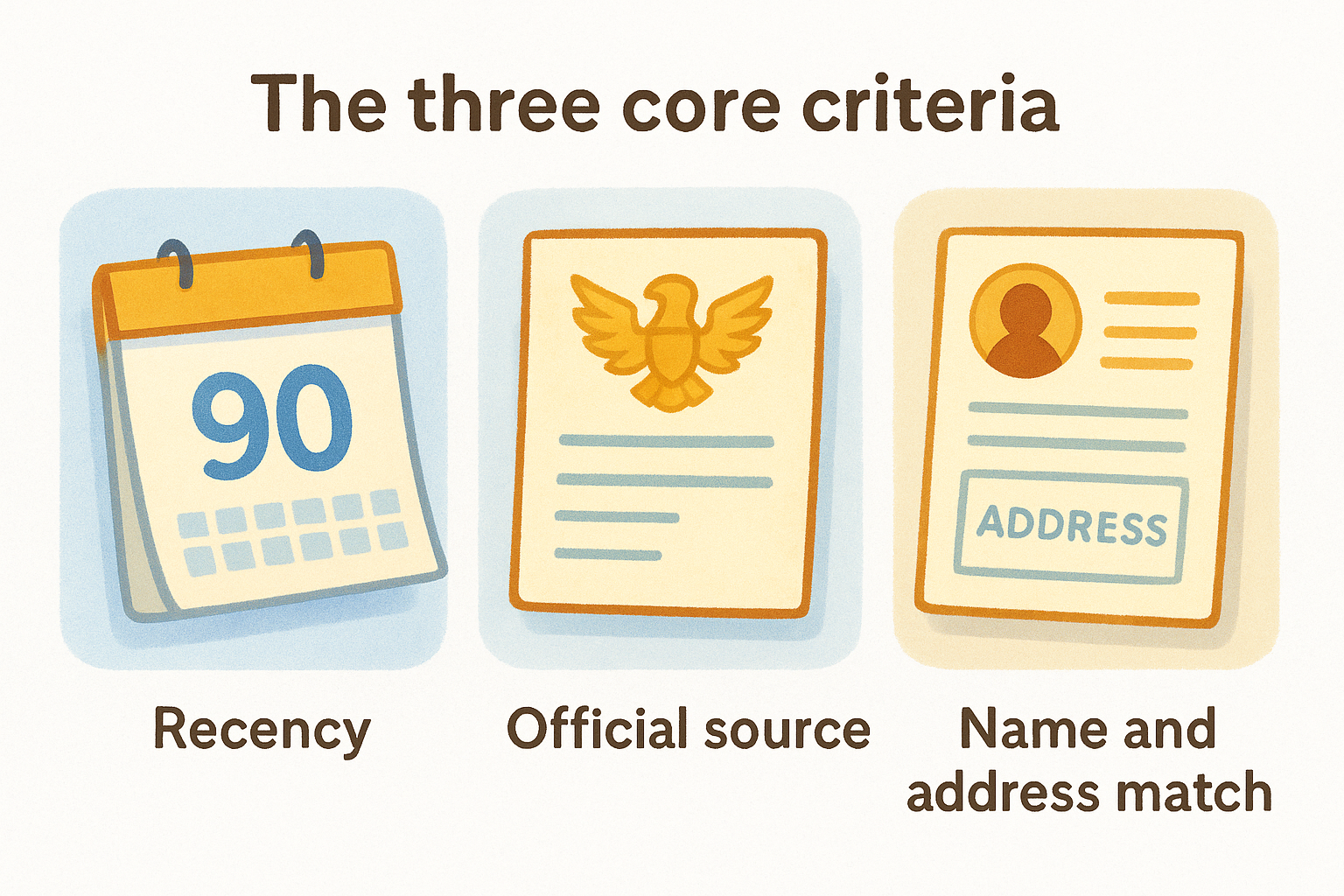

The three core criteria

Most banks, DMVs, and government agencies evaluate address documents against three basic requirements: how recent the document is, who issued it, and whether it displays your full legal name alongside your current address clearly.

- Recency: Most institutions require documents issued within the last 90 days, though some accept up to 12 months for certain document types like government-issued letters.

- Official source: The document must come from a recognized issuer such as a government agency, utility provider, or licensed financial institution.

- Name and address match: Your full name and address on the document must exactly match the information you provided on your application.

If any detail differs from your application, even a missing middle initial, institutions will typically reject the document and ask you to resubmit.

Common acceptable proof of address documents

The list of acceptable documents for proof of address is broader than most people expect, but it breaks cleanly into two categories: government-issued records and financial or utility documents. Knowing which category your institution prefers saves you from an unnecessary back-and-forth.

Government-issued documents

Government records carry the highest level of credibility with banks and the DMV because they come from verified public databases. Most institutions accept these without question when they display your full name and current address.

- State-issued driver's license or ID card

- U.S. passport or passport card

- Voter registration card

- Tax assessment notice or IRS correspondence

- Social Security correspondence

Government-issued documents rarely get rejected for recency if they are still active and valid, making them the most reliable option to submit first.

Financial and utility documents

Bank statements, mortgage statements, and utility bills are the most commonly submitted documents in this category. Your utility bill from an electric, gas, water, or internet provider works at nearly every institution, provided it is dated within the last 90 days. Lease agreements signed by a licensed landlord and credit card statements from major issuers also qualify in most cases.

What to do if you don't have utility bills

Not everyone has a utility bill in their name, especially if you rent a furnished apartment, live with family, or recently moved. That does not mean you are out of options. There are several practical alternatives that qualify as acceptable documents for proof of address at most institutions.

Use bank or government records instead

Your bank statement or mortgage statement works at nearly every institution and is often easier to access than a utility bill. Log into your online banking portal and download a PDF statement from the last 90 days. Government correspondence such as an IRS tax notice or Social Security letter also carries significant weight and rarely gets rejected.

If you receive statements digitally, most institutions accept a printed PDF as long as it comes from an official online account portal and is not manually edited.

Request a letter from your landlord or employer

If your name is not on any bills, a signed letter from your landlord confirming your residence works in many situations, particularly at banks and credit unions. Some institutions also accept an employer-issued letter on official letterhead that confirms your home address. Call ahead to confirm the format the institution requires before submitting either option.

How to submit proof of address without delays

When you submit acceptable documents for proof of address, the format matters just as much as the document type itself. Institutions regularly reject valid documents because of poor image quality, cropped edges, or missing pages, not because the document was wrong. Getting this right the first time prevents weeks of back-and-forth with compliance teams.

Prepare your documents before you apply

Before you upload or bring in any paperwork, check that your name and address match exactly what you entered on your application. Even a minor discrepancy like an abbreviated street name can trigger a rejection. Confirm the document date falls within the institution's required window, which is typically 90 days for most banks and DMV offices.

A blurry photo taken at an angle is one of the most common reasons institutions flag a submission for manual review.

Submit the right format the first time

Most institutions accept digital PDFs downloaded directly from your bank or provider's portal, which are consistently cleaner than photographed physical copies. If you submit in person, follow these steps to avoid common delays:

- Bring the original document, not a photocopy

- Confirm the institution accepts your specific document type before traveling

- Ask for a receipt or confirmation number after submitting

Quick recap and next step

Knowing which acceptable documents for proof of address qualify at banks, the DMV, and crypto exchanges puts you ahead of most applicants. Government-issued records and recent financial statements cover the vast majority of verification requirements, and alternatives like landlord letters or employer correspondence fill the gap when standard utility bills are not available.

Submitting the right document in the right format, with your name and address matching exactly, is what separates a fast approval from weeks of back-and-forth with a compliance team. Following the steps in this guide gives you a clear path through the process, whether you are opening a bank account, updating your license, or completing KYC on a crypto platform.

Once your identity is verified, the next step is learning how to actually protect the assets you hold. Start building that knowledge today through the FinTech Dynasty crypto education course, designed to take you from basic concepts to secure self-custody.